简体中文

简体中文

100 U.S. dollar banknotes. /Getty

Editor's note: Huang Yongfu is an economic affairs commentator. After completing his Ph.D., he began his career at the University of Cambridge and then moved on to the UN system. He is an author of many papers and books on economics. His current interests lie in global development and Sino-U.S. links, especially trade, financial and technological issues. The article reflects the author's opinions and not necessarily the views of CGTN.

To deal with the downturn wrought by the COVID-19 pandemic, U.S. President Joe Biden, in his first 100 days, unveiled the most ambitious left-wing agenda in history in terms of a massive expansion of the federal government and unsustainable spending increases. His new federal spending for the next decade includes a $1.9-trillion COVID-19 relief package, $2.3-trillion green energy and infrastructure bills, and $1.8-trillion American Families Plan, on top of the regular federal budget of more than $4 trillion a year.

Can Biden's economic stimulus break the U.S. economy out of the low-rate and low-inflation trap, and even get the U.S. economy to take off in the 21st century?

The macroeconomic policymaking characterized by lower taxes plus deregulation, laid out by Ronald Reagan in the 1980s and which lasted for four decades, has been regarded as the best formula for faster growth and broadly shared prosperity.

In the wake of the 2007-09 crisis, under the new label of "quantitative easing," the Federal Reserve has printed the most common measure of money by a factor of three, even by quadruple, amid the outbreak of the COVID-19 to buy government bonds. Inflation is yet to appear. The Fed has kept signaling not to raise interest rates until inflation is "on track to moderately exceed 2 percent for some time."

According to John Maynard Keynes's General Theory, in a liquidity trap when interest rates can go no lower, fiscal policy is the most effective way to boost the economy because of its sizeable "multiplier" effect. To fight COVID-19, most mainstream macroeconomists inclusive of the IMF have called for aggressive fiscal policies.

President Biden's economic proposals represent a major shift in macroeconomic policymaking. Opposing the non-Keynesian view that policymakers should just defer to markets, the Biden administration is pursuing a Keynesian approach to redefine a muscular government role in shaping the economy, more specifically by fine-tuning aggregate demand via huge public spending and taxation.

Biden's stimulus emulates and combines most of his predecessors' government-directed programs, such as the modern government-funded social safety net created by Franklin D. Roosevelt in the 1930s, the interstate highway system initiated by Dwight D. Eisenhower in the 1950s, and the federal industrial policy set up by John F. Kennedy in the 1960s.

Contrary to his predecessors' timidity during the 2007-2009 crisis, Biden is being bold, and letting rip somewhat. It's no surprise that his huge stimulus has been rightly criticized as "incontinent," with well over half of it free handouts to individuals.

While pent-up household savings could result in consumer demand rising and more general inflation, innovation and work ethic would be compromised where Americans are rewarded for either not working or wage increases that add to inflation. The confiscatory tax increases would seriously damage the economy, by punishing savings and making U.S. businesses less competitive abroad.

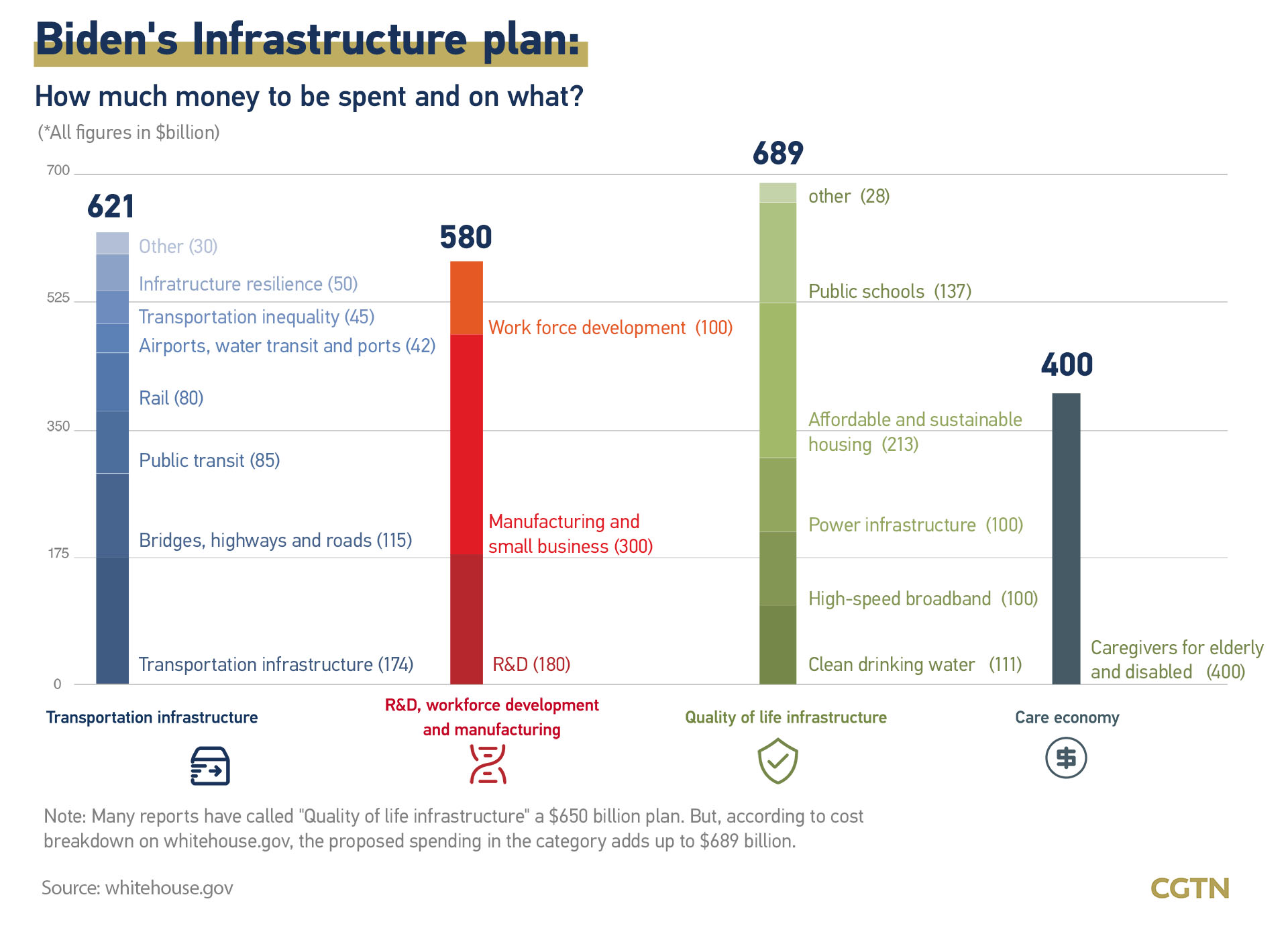

Graphics: Biden's infrastructure plan. /CGTN

Worse still, Biden's unprecedented stimulus features historic levels of government debt, billing the fiscal difference to future generations. From 1970 onward, the U.S. has shifted from a balanced-budget policy to a budget-deficit policy in the sense of spending more than current revenue as a matter of routine. As COVID-19 panicked markets, by the end of 2020, total fiscal stimulus has already amounted to almost $3 trillion (about 14 percent of GDP in 2019). The public deficit in 2020 ballooned to nearly half of spending, mainly due to the pandemic, from 10 percent in the 1970s and 18 percent in the 1980s.

Biden's stimulus is a big gamble. The risk of confidence crises could be most dangerous for the growing public debt. When a self-fulfilling panic causes prevalent pessimism, the change can come suddenly and without warning, and shifts in investors' risk appetite can be overwhelming. The subsequent confidence crises can provoke runs on the growing government debt.

In his new book entitled "Value(s)," Mark Carney, former governor of the Bank of England, points out that "trust is central to maintaining the stability of a currency or a financial system" and self-interest crowds out other motivations, making the world a potentially more selfish and less resilient place to live.

One potential area of risk could emerge from the geopolitical conflict. Recently, the U.S. Senate Foreign Relations Committee has passed the "Strategic Competition Act of 2021," a legislative blueprint that frames China as its strategic competitor. It claims without evidence that whatever development policies pursued by China are "contrary to the interests and values of the United States, its partners, and much of the rest of the world," which is ridiculous. While its title implies a policy of "strategic competition" with China, the bill doesn't actually propose anything that would legitimately advance competition. Instead, it includes various military or media financing, for example, an annual $300 million to fund and train media that reports on the "negative impact" of the Belt and Road Initiative.

Perils lurk as soon as geopolitical competition bites. Lingering geopolitical risks will sap the confidence of investors, ignite demand fears and bank runs, and eventually alter the pitch of Biden's stimulus.

To fulfill his ambition to reinvigorate the U.S. economy in the 21st century, President Biden shouldn't be hijacked by elite interests with a dilapidated ideology when it comes to China.

(If you want to contribute and have specific expertise, please contact us at [email protected].)